Your systems worked on their own. Now how do they work with each other?

You’ve both been independent for your entire adult lives and have managed to do okay financially. You’ve chosen each other. But now it’s time to talk about money. The rent is due, you just got your first utility bill, your student loans are coming up, and you’ve got to figure out what it all means for the both of you. You pull up your favorite app, your partner brings up their go-to spreadsheet, and you both look at each other like you speak different languages. Your systems worked on their own. Now how do they work with each other?

This is the part nobody warns you about. The easy move is to let the person who’s most competent, or at least most insistent, take the wheel. It works until it doesn’t. Until one of you is left guessing what’s in the accounts, what’s owed, what you’re saving for, or what would happen if the other one couldn’t manage it tomorrow.

We’ll walk through the three common models couples use to structure their finances together. But the model is only the scaffolding. How you structure your money matters less than whether both of you can see it, discuss it, and plan together effectively.

Models Couples Use to Combine Finances

Fully Combined Finances (“Ours”)

In this setup, all income from both partners is deposited into joint accounts, and all expenses, bills, and savings are paid from this shared pool. This method streamlines budgeting and fosters a strong sense of teamwork and transparency. However, it reduces individual autonomy and can create tension or resentment if partners have different spending habits. In situations where one partner is the financial manager, the other partner can be left feeling completely powerless. Since every dollar spent is visible, personal purchases, like hobbies, clothing, or even surprise gifts for the other partner, can feel scrutinized. To navigate these drawbacks, couples using the Ours system may rely on:

- Big Purchase Rule: Any unilateral, non-essential spending above a certain threshold requires discussion before the purchase is made

- Allowances: Agreed-upon amounts of spending money built into the budget for each partner to allow them to maintain a sense of freedom without the need to check in.

Fully Separate Accounts (“Yours & Mine”)

Partners maintain completely separate bank accounts and divide their shared bills. Couples using this method usually split expenses in a few ways:

- 50/50 Split: Each partner pays exactly half of the shared expenses. This is straightforward but can feel unfair and cause resentment if one partner earns significantly more than the other.

- Proportional Split: Partners contribute a percentage of the shared bills that matches their share of the total household income (e.g., if one earns 70% of the household income, they pay 70% of the bills).

- One Pays All, Other Reimburses: One partner pays all shared bills upfront, and the other reimburses them for their portion at the end of the month.

- Expense Segregation: One partner’s income is dedicated entirely to monthly living expenses, while the other partner’s income is routed directly into savings and investments.

The Hybrid Approach (“Yours, Mine & Ours”)

This is a popular middle ground where couples maintain both joint and individual accounts. There are multiple ways partners make this work:

- Equal Contributions: Each partner contributes an equal amount to the joint accounts to meet their household budget. This can work if both partners have similar incomes, but it can be overly burdensome and unfair if there is a large disparity between incomes.

- Proportional Contributions: Each partner contributes to the joint accounts proportionally, (e.g. if one partner makes twice as much as the other, then they contribute twice as much to the joint accounts)

- Personal Allowance: Partners each contribute every dollar above a certain personal allowance to the joint accounts and keep the allowance in their own personal accounts.

Beyond Models

The Importance of Visibility & Coordination

There are couples who have fully shared accounts, but one partner couldn’t tell you how much the mortgage or electricity bill is nor when they are due.

Strong opinions exist about which model is best. We’re not going to add to them, because the model isn’t actually what determines whether this works. What matters more than the model itself is having both partners involved and on the same page about the current status of their finances and future plans. This takes work regardless of how things are split and which accounts money lives in. There are couples who have fully shared accounts, but one partner couldn’t tell you how much the mortgage or electricity bill is nor when they are due.

The risks that come with partners not being aligned include:

- Disempowerment: One partner doesn’t know what they have, what they owe, or what would happen if they had to manage it tomorrow.

- Overload: One partner feels exhausted and potentially unappreciated for being the manager of the finances.

- Unpreparedness: When tragedy strikes and one partner passes or is incapacitated for a period of time, the other partner is not in a position to effectively take over and the result is chaos.

How Deena Helps

Deena’s flexibility supports any model you choose, and it has core features which help you communicate, plan, and coordinate your finances as a couple.

Mine & Ours Households

Deena is fundamentally built with the household as a core container for all of your concerns. You are allowed to create as many households as you see fit to organize your life and share any of them with other people. That means you can create a Mine household, your partner can create their Yours household, and each of you can connect only your personal financial accounts, create your personal budgets, and manage any financial goals you have separately from each other. You can also create an Ours household, which you connect your joint accounts to, plan your household budget in, and make shared plans for the future.

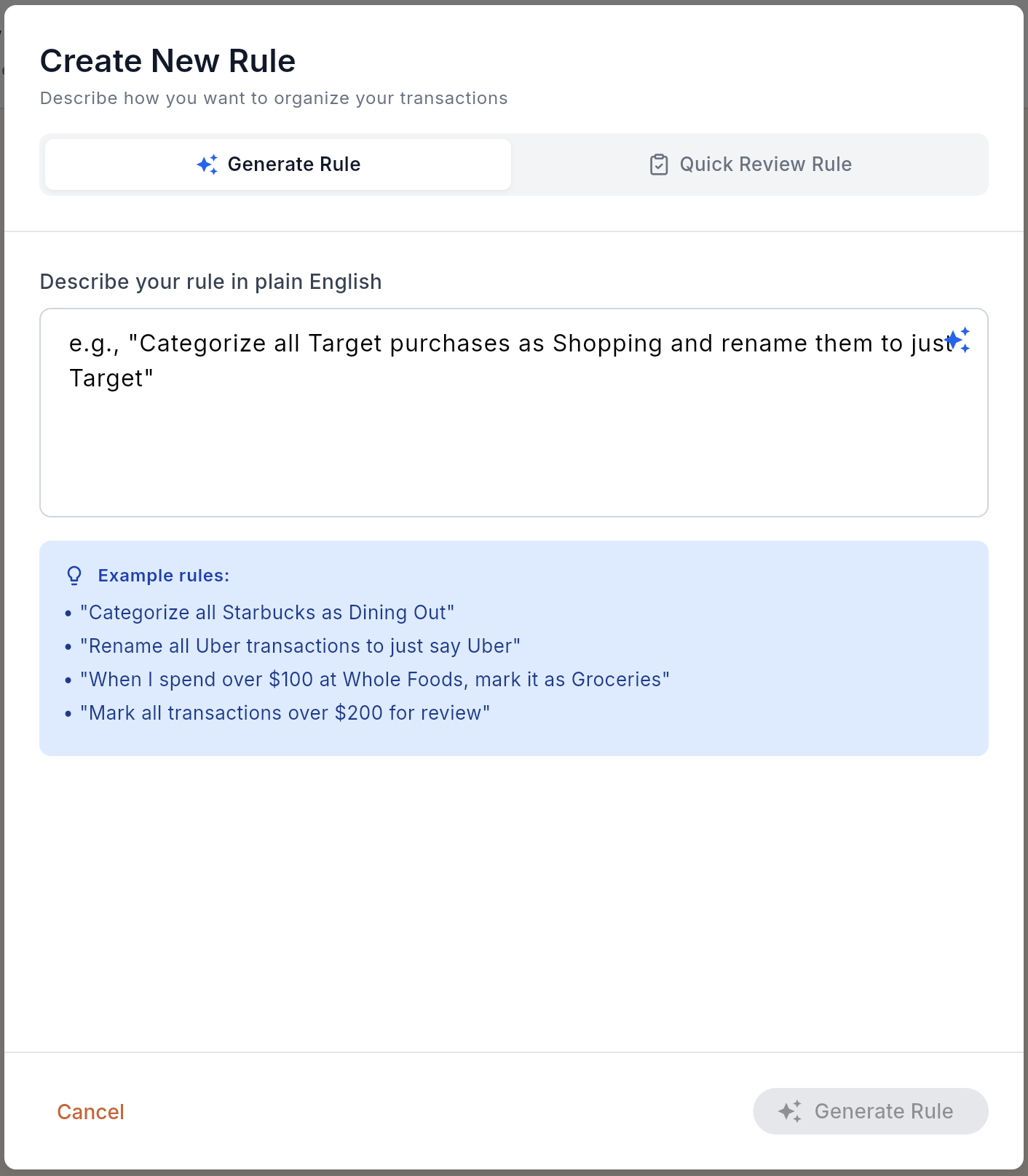

Budget Alerts & Transaction Review Rules

Deena allows you to create a household budget and set budget alerts which let you know when your spending in a category is reaching or has surpassed the set limit. We also allow you to create rules that certain transactions should be reviewed by any or a specific member of the household. This helps to provide the financial visibility required to stay on the same page and monitor the current state of your finances together.

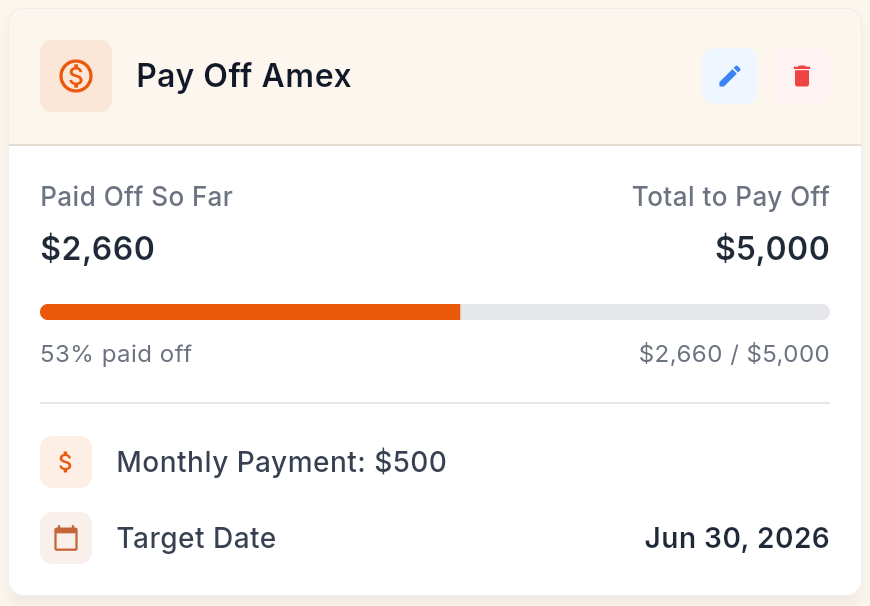

Financial Goal Tracking

Deena allows you to create financial goals for your household, including Savings or Debt Reduction goals. You can link these goals to a financial account and automatically track your progress against them. Deena will let you know when your goal is looking like it might be off-track and provides suggestions for what to do. This way you and your partner can stay in sync about where you’re headed financially.

The Check-in

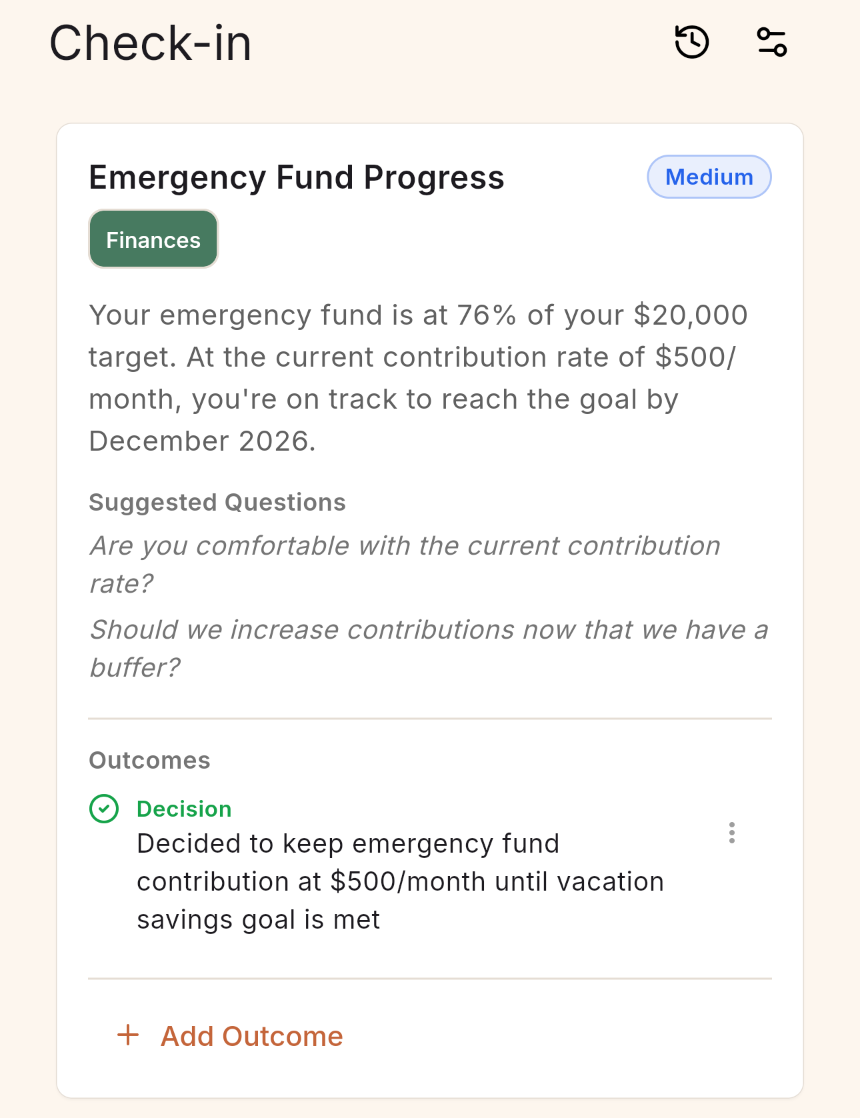

It is important that regardless of what system you use, you and your partner communicate regularly about finances to assess where you are, adjust budgets, set goals, and give each other peace of mind. This is called a Money Date and Deena supports this with the Check-in feature.

Check-ins analyze the state of your household regarding any set of topics you choose and creates an agenda for you and your partner to discuss together. It also provides a place for you to record decisions and action items which serve as a living record, so neither of you have to be confused about what you talked about or planned. Action items become tasks that you can track using the Tasks feature. This provides clarity and accountability for you and your household.

Getting Started

The hardest part of merging finances isn’t the model — it’s starting the conversation. Make sure you and your partner are speaking the same language. Pick a time this week, sit down together, and talk through which model fits where you are now. Then set up the infrastructure that makes visibility automatic instead of effortful.

Sign up for your Deena free trial today, and our onboarding process will walk you through setting up your first household together.